Budgeting Smarter on a Fixed Income: Enjoy More, Stress Less

Living on a fixed income doesn’t have to mean cutting joy; it just means giving your dollars a clearer job. With a few small tweaks, you can reduce money stress, reduce risk to your savings, and still make room for the people, places, and hobbies you love.

Start with a one-page money snapshot

● List your monthly income (Social Security, pension, annuities) and essential costs (housing, utilities, groceries, transportation, insurance, medical).

● Track three numbers monthly: cash on hand, total debt, and total savings/investments.

● Name your top three priorities for the year (e.g., a trip, grandkids’ activities, home repairs). Let these guide what you keep and what you trim.

Build “buckets” you can actually follow

Create three easy accounts or budget categories:

- Essentials – bills on autopay

- Everyday – groceries, gas, small purchases

- Joy & Goals – travel, gifts, hobbies

Automate transfers on deposit day. When the primary bucket runs low, you'll see it before you overspend.

Trim costs that don’t hurt

● Re-shop home/auto insurance annually; ask about safe-driver and bundle discounts.

● Audit subscriptions and memberships each quarter; keep what you use, cancel the rest.

● Switch a few meals to low-cost anchors (soups, omelettes, beans-and-rice bowls).

● Enroll in budget billing for utilities to smooth seasonal spikes.

How to lower your insurance costs

● Shop around once a year and get at least three comparable quotes; ask each carrier to match your best offer.

● Bundle home and auto where it truly saves; verify the combined premium beats separate policies.

● Raise deductibles to a level you can comfortably cover from your emergency fund.

● Trim extras you don’t use (towing, rental, device insurance) and avoid duplicate coverages across policies.

● Earn discounts with proof: defensive-driving course, claims-free status, safe-driver telematics, smoke/CO detectors, water-leak sensors, or a monitored alarm.

● Pay in full or use automatic payments to reduce installment fees; keep a strong on-time payment history.

● Review coverage amounts annually—adjust for current home value, mileage driven, and life changes (retirement, downsizing).

● For health coverage, recheck your plan during open enrollment, confirm your medications are on the formulary, and ask providers about generics or in-network options.

● Maintain strong credit; many states allow insurers to use credit-based insurance scores that influence premiums.

Consider converting existing insurance into cash

If you own a life insurance policy you no longer need or can’t comfortably afford, selling it can sometimes create a cushion for living expenses and care. Understanding the role of a life settlement broker is key: brokers advocate for you (the policyholder), not buyers, and market your policy to multiple licensed investors—creating competition instead of steering it to one purchaser. Ask about fees, how many bids they’ll obtain, estimated net proceeds after taxes, and any impact on benefits like Medicaid before moving forward.

Make healthcare predictable

● Use preventive care and ask your pharmacist about generic alternatives.

● During Medicare open enrollment, verify that your medications are on your plan’s formulary.

● Build a small “medical buffer” fund (one month of essentials) to cover co-pays and surprise bills.

Guard against leaks and scams

● Freeze your credit at all three bureaus; thaw only when needed.

● Use a password manager and turn on two-factor authentication.

● If someone demands gift cards, crypto, or a wire transfer, it’s a scam—hang up and call the official number.

Keep joy in the plan

Frugal ≠ joyless. Budget for small delights: free concerts, library events, walking clubs, potlucks, community classes. Pick one meaningful splurge each quarter (a day trip, a class, or a special dinner) and save toward it in your Joy & Goals bucket.

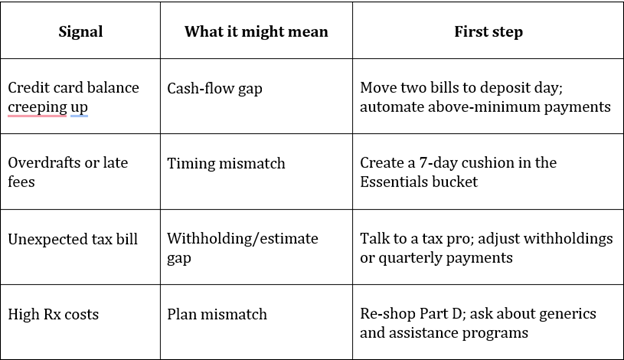

Quick table: signals and first steps

Checklist to stretch every dollar

☐ Separate banking for Essentials, Everyday, and Joy & Goals

☐ Automate bill pay and savings on deposit day

☐ Freeze credit and enable two-factor authentication

☐ Review Medicare plan and prescription coverage annually

☐ Re-shop insurance once a year

☐ Cancel one unused subscription this month

☐ Schedule a quick monthly money check-in (15 minutes)

Easy ways to spend less without feeling it

● Shop with a list and eat before you go; leads to fewer impulse buys

● Use senior discounts for transit, museums, and community classes

● Borrow from the library instead of buying new books or streaming rentals

● Batch-cook and freeze portions to reduce waste and takeout

A two-week starter plan

Week 1

● Make your one-page snapshot and set up three buckets.

● Put bills on autopay and schedule transfers for deposit day.

● Freeze your credit and change two weak passwords in your manager.

Week 2

● Re-shop one insurance policy and review your Medicare meds list.

● Plan two low-cost dinners; redirect the savings to Joy & Goals.

● If a life policy no longer fits, schedule a call to learn about brokered settlement options and get clarity on net proceeds and benefits impact.

Final word

Favorable budgets are simple, automated, and aligned with what you value. Get your buckets flowing, protect against avoidable leaks, and explore creative cash sources—generally when they make sense. With a calm monthly rhythm and a few smart levers, your fixed income can fund a rich, steady life filled with the people and moments that matter most.

References

“How to Prioritize Your Financial Goals: Saving vs. Paying Off Debt,” Transcend Credit Union. Accessed online 4 Dec 2025. https://www.transcendcu.com/how-to-prioritizeyour-financial-goals-saving-vs-paying-off-debt

“How to bucket your money,” by Kelly Simpson. Spaceship Capital Limited. Published online 23 Sept 2025. https://www.spaceship.com.au/learn/how-to-bucket-your-money/

“Find Defensive Driving Discounts & Courses by State,” Geico. Accessed online 4 Dec 2025. https://www.geico.com/save/discounts/defensive-driver-discounts/ “Bean and rice bowls,” by Kathryn Doherty. Family Food om the Table. Modified 11 Mar 2025; Published 18 Feb 2021. https://www.familyfoodonthetable.com/bean-and-ricebowls/

“5 Ways to Make Sure Your Home is Insured to Value,” Mutual Benefit Group. Accessed online 4 Dec 2025. https://www.mutualbenefitgroup.com/insurance-101/personalinsurance-101/insure-to-value

“Life Settlement Brokers: Why Independence Matters,” Windsor Life Settlements. Accessed online 4 Dec 2025. https://windsorlifesettlements.com/life-settlement/life-settlementbrokers/

“Retirees, Don’t Miss Out: Must-Know Medicare Open Enrollment Tips,” By Maurie Backman. 24/7 Wallstreet. Published 15 Oct 2025. https://247wallst.com/investing/2025/10/15/retirees-dont-miss-out-must-knowmedicare-open-enrollment-tips/

“Top 10 Scams Targeting Seniors,” Georgia Attorney General’s Consumer Protection Division. Accessed online 4 Dec 2025. https://consumer.georgia.gov/top-10-scamstargeting-seniors

“8 health benefits of exploring new places,” Push Doctor. UK NHS. Accessed online 4 Dec 2025. https://www.pushdoctor.co.uk/exercise/8-health-benefits-of-exploring-new-places

Photo from Freepik

Disclosure: Investment advisory and financial planning services are offered through Simplicity Wealth, LLC, an SEC-registered investment adviser. SEC registration does not constitute an endorsement of the firm nor does it indicate that the advisor has attained a particular level of skill or ability. Insurance, Consulting, and Education services are offered through Rhoads Agency. Rhoads Agency is a separate and unaffiliated entity from Simplicity Wealth. This material is intended for educational purposes only and is not intended to serve as the basis for any purchasing decision. This information is provided as general information and is not intended to be specific financial guidance. Before you make any decisions regarding your personal financial situation, you should consult a financial or tax professional to discuss your individual circumstances and objectives. Any information provided may result in contact by an insurance agent. The source(s) used to prepare this material is/are believed to be true, accurate and reliable, but is/are not guaranteed.